The de-escalation in Iran and the move to new highs confirm that markets had already priced in the next phase before it was reflected in the data.

In markets, confirmation does not come when an estimate is made. It comes when the scenario begins to materialize, while the majority continues to question it.

In the previous period, we highlighted that the tension surrounding Iran and the energy shock had already been largely priced in by the markets, and that the next phase would be characterized by stabilization and a return of upward momentum. This approach was based on the behavior of capital flows, the divergence in performance, and the inability of energy prices to validate a scenario of sustained escalation.

The evolution of events confirmed this assessment. The gradual de-escalation of the crisis in Iran and the absorption of the energy shock led to a restoration of confidence and a clear shift of capital toward risk assets. Major indices moved toward new highs, confirming that the phase of fear had already been completed before the official de-escalation was recorded.

Importance should also be given to the confirmation of the effectiveness of the extension strategy followed by Donald Trump, which we had identified as a key mechanism for market stabilization. Developments confirm that giving markets time acts as a catalyst for absorbing risk, limiting the intensity of reactions and creating the conditions for a gradual restoration of confidence.

This move does not mark the end of the cycle, it marks its beginning. At the same time, a series of additional developments reinforce the transition to a new phase. Expectations of stabilization in U.S. monetary policy are already supportive for risk assets, while the resilience of the dollar confirms that international capital continues to flow into the American market. At the same time, there is a noticeable increase in allocations to sectors linked to the real economy, such as transportation and infrastructure, a trend that is directly connected to the dynamics of shipping.

Equally important is the gradual stabilization of the Chinese economy, which supports demand prospects for commodities and transportation, creating a more favorable environment for global trade.

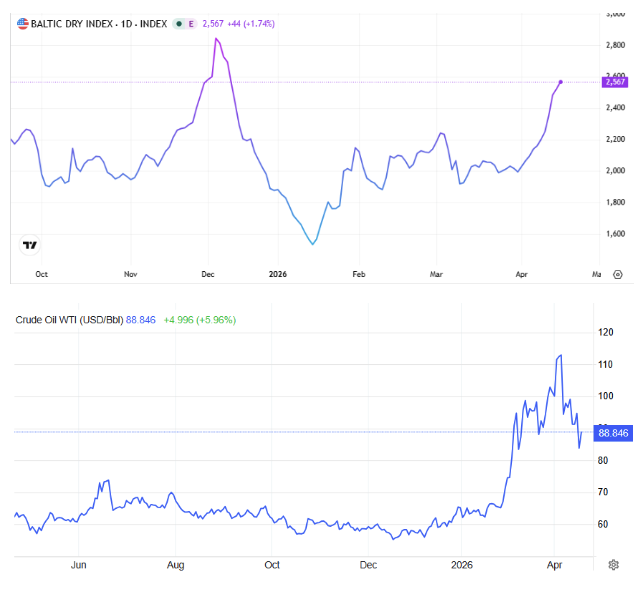

At the same time, the behavior of the energy market confirms the shift in direction. The inability of oil to move to new highs, combined with the sharp correction in products such as gasoil, suggests that the recent energy rally had the characteristics of a short-term shock rather than a sustainable trend.

The limited increase in volatility confirms that markets treated the crisis as a manageable event rather than a systemic risk.

The structure of the market is already beginning to change. The first phase of the move was driven by energy and commodities. The next phase is expected to be characterized by broader participation, with the technology sector maintaining strong momentum and reasserting its role as a key driver.

At the same time, shipping is entering a particularly favorable environment. The easing of energy costs, combined with sustained demand and the restructuring of trade flows, is creating conditions that have historically led to strong upward phases for the sector.

The confirmation of new highs is not merely a technical development. It is an indication that markets have moved from a phase of uncertainty to one of confidence.

Based on the developments so far, we estimate that the coming months are likely to reinforce the positive factors that have already begun to take shape. The stabilization of the geopolitical environment, the easing of energy costs, the resilience of the U.S. economy, and the gradual improvement in global expectations create a backdrop that supports the continuation of upward momentum. In this context, the current phase is far from a market peak and is better understood as an intermediate stage within a broader upward cycle that is unfolding.

Market experience shows that “good news” does not mark the beginning of an uptrend but rather confirms that it has already started. In previous cycles, the gradual easing of geopolitical tensions, the stabilization of monetary policy, and the decline in energy pressures marked the transition from the pricing phase to the acceleration phase. The same pattern is beginning to emerge today.

The de-escalation in Iran, the resilience of key macroeconomic indicators, and the return of indices to an upward trajectory are not isolated developments, but elements of a broader shift in direction. Historically, when such conditions align, markets tend to enter phases where the rally gains both breadth and duration, as participation expands and capital moves more aggressively toward risk.

At the same time, our assessment of the strength of the shipping sector has also been confirmed, with the upward movement of the Baltic Dry Index toward its previous highs, unfolding in line with the scenario we had outlined. Our approach was based on the view that the sector’s positive fundamentals are not solely linked to geopolitical tension, but to deeper structural changes in trade flows and transportation demand. This development confirms that even in a scenario of de-escalation in Iran, shipping maintains its upward momentum, acting as an early indicator of broader economic activity and the next phase of the global cycle.

The Baltic Dry Index has historically functioned as a leading indicator of the real economy, anticipating changes in demand before they are reflected in macroeconomic data — a role that, in our view, is being clearly reaffirmed in the current environment.

In this context, the recent positive developments should not be interpreted as a delayed reaction, but as an early confirmation that the next upward phase is already underway. And as has repeatedly been the case in the past, markets do not wait for full clarity before moving ahead of it.

by Kotsiakis George