Markets are moving from pricing to acceleration, as earnings, the Fed and geopolitical developments begin to align.

Catalyst: 700 companies (with a combined market cap of $45 trillion) report earnings this week.

Fed Pivot: The transition from Powell to Warsh brings expectations for faster easing.

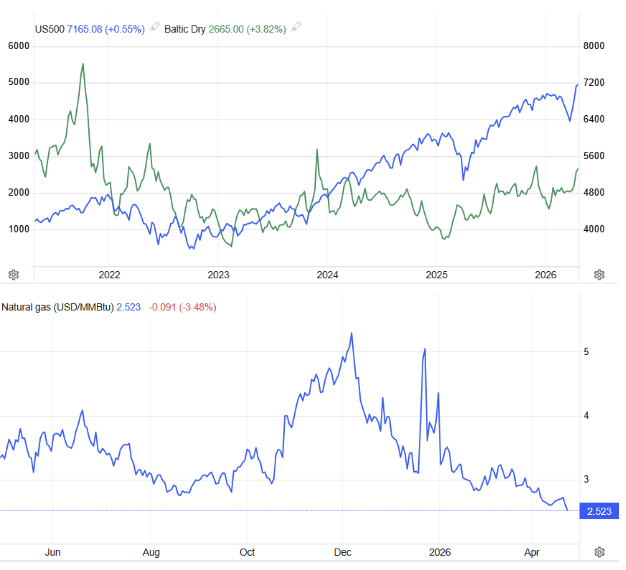

Shipping Alert: The BDI signals “overheating” demand, targeting 3,000 points.

Geopolitics: The 60-day “War Powers Resolution” window is shifting from a risk factor into a political stabilization tool.

As Wall Street completed a week hovering near its all-time highs, the calm on the board appears deceptive. This is not stagnation, but the “calm before the storm”, a storm of positive catalysts. We are at ground zero, where blockbuster corporate earnings, a historic leadership transition at the Fed, and the geopolitical chessboard are aligning. The pricing-in phase is over. The acceleration phase has just begun.

Markets continued this week to trade near their highs, confirming that the underlying momentum remains bullish despite ongoing geopolitical uncertainty. At the same time, oil prices moved clearly in line with developments surrounding negotiations and statements regarding a potential meeting between the United States, Iran, Israel and Lebanon, as well as the progress of ceasefire discussions. The picture of recent days confirms that the main driver of the markets is no longer the conflict itself, but the probability of a political resolution, and above all, its timing.

The coming week takes on particular importance, as it brings together a rare combination of catalysts capable of shaping market direction. On the corporate front, some of the world’s most important companies, including Alphabet, Apple, Microsoft, Amazon, Meta, Visa and Mastercard, along with major energy companies, are reporting results. The market is now called to confirm whether the $23 trillion in market capitalization they represent justifies current valuations, at a time when the total capitalization of the U.S. market stands at approximately $64 trillion. In total, 700 companies with a combined market capitalization exceeding $45 trillion are reported. If results confirm expectations for a sixth consecutive quarter of growth, the “acceleration” we refer to will evolve into an unstoppable bullish cycle, making this the most critical earnings week of the period.

One of the most critical elements of the current phase is the behavior of capital. Despite heightened geopolitical uncertainty, there has been no mass exit from risk assets, but rather a reallocation of positions. Flows initially moved toward energy and commodities and are now gradually returning to equities. This confirms that investors did not abandon risks, they simply repositioned it, a pattern historically associated with transitional phases rather than market weakening.

At the same time, the Fed meeting takes on particular significance, as it effectively marks the end of an era under Powell and the transition into a new phase of monetary policy. The market is no longer focused solely on the immediate interest rate decision, but primarily on the signal for what comes next. With Powell’s term ending on May 15, 2026, and Kevin Warsh’s candidacy gaining traction (following the withdrawal of DOJ investigations), the market is already pricing in a more aggressive shift toward lower rates. The key question is whether the next leadership, once again a selection under the Trump administration, as Powell was in his first term, will move more aggressively toward easing, as President Trump has indicated, and as Miran - also a Trump appointee - has been voting in recent meetings. Historically, such transitions act as turning points, directly impacting liquidity and risk appetite.

At the same time, the behavior of volatility confirms the resilience of the market. Unlike previous geopolitical crises, the increase did not remain limited and instead moved toward higher levels, indicating that investors did not treat the situation as a systemic risk. Its rapid normalization reinforces the view that the shock has already been absorbed.

On the geopolitical front, we are approaching the 60-day mark since the start of the military engagement in Iran, as defined by the War Powers Resolution. While formal approval from Congress is technically required beyond this point, history shows that this threshold functions more as a political pressure mechanism than a real constraint. From Kosovo to Libya, past U.S. administrations have repeatedly operated beyond this framework, turning the deadline into a negotiation tool.

In the current environment, the strategy of extensions acts as a mechanism of de-escalation rather than escalation, increasing the likelihood of reaching an agreement or some form of stabilization. For markets, this means that geopolitical risk is gradually shifting from a threat into a catalyst.

The structure of the market is already beginning to change. The first phase of the move was led by energy and commodities. The next phase is expected to be characterized by broader participation, with the technology sector maintaining strong momentum and reclaiming a leadership role. Historically, major bull cycles are accompanied by strong technology leadership, reinforcing the probability of continued upside.

While most focus on technology, the real economy is sending signals through the sea. The decline in energy costs, combined with the restructuring of trade flows, places shipping at the forefront.

Our view is clear: the Baltic Dry Index has the potential to break above the 3,000-point level in the near term, confirming that demand remains strong despite geopolitical challenges.

Both the Baltic Dry Index and the Dow Jones Transportation historically act as leading indicators of the real economy, anticipating shifts in demand before they are reflected in macroeconomic data, a role that is clearly being confirmed once again in the current phase.

Historical experience shows that markets react more intensely before events than during them. In cases such as the Gulf War and the Iraq invasion, the greatest pressures occurred before the start of military operations, while the period that followed was characterized by stabilization and a strong upward reaction. The same pattern appears to be unfolding today.

In our view, we are precisely at this stage. At a point in time where developments have the potential to trigger a very strong upward movement in the markets. In this environment, the question is not whether the market is expensive or whether risk exists. The question is timing. When earnings, the Fed and geopolitics align, the market does not simply continue higher, it accelerates aggressively. And in such periods, the critical question for investors is not what has already happened, but where they choose to be positioned.

The key question for investors remains one:

Will you be part of the move, or merely observers of it?

by Kotsiakis George