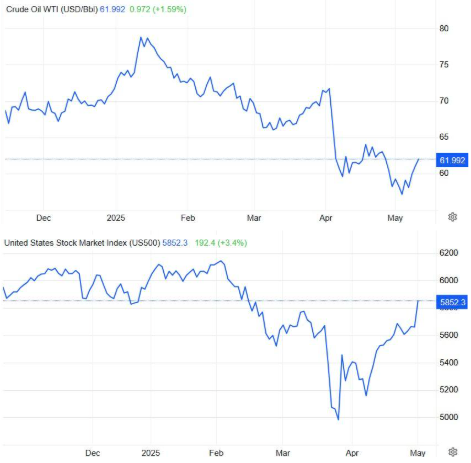

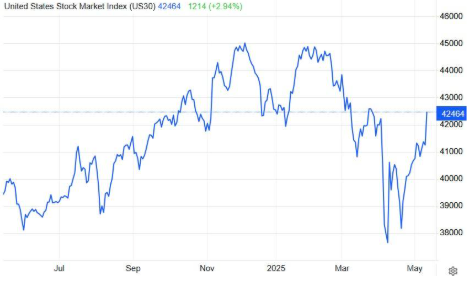

Today's article comes one month after President Trump announced the 90-day extension on tariff implementation, and the market picture continues to show the same contradictions — with Europe recording significant gains of over 15% and the U.S. facing losses close to 10% — as it has since President Trump’s inauguration. However, there are now some notable differences compared to what many critics had claimed: that the President of the United States acts against American interests and lacks concern for market performance.

The sharp decline in U.S. indices began around March 24–26, 2025, with the following detailed performance:

- Dow Jones (03/26–04/07): -14.20%

- S&P 500 (03/26–04/07): -17.10%

- Nasdaq (03/26–04/07): -19.90%

- Russell (03/26–04/09): -19.60%

- Dow Transportation (04/02–04/08): -17.00%*

*We include this index in our analysis as the transportation sector is a key indicator of economic health and growth, reflecting the movement of goods and products.

From April 9, 2025 — when the tariff extension was officially announced — until the time of this writing, market performance has reversed sharply:

- Dow Jones (04/07–05/12): +15.95%

- S&P 500 (04/07–05/12): +18.60%

- Nasdaq (04/07–05/12): +27.40%

- Russell (04/09–05/12): +17.60%

- Dow Transportation (04/09–05/12): +20.60%*

The S&P 500, Nasdaq, and Dow Transportation indices are now trading at or above their levels of March 26, when the decline began, while the Dow and Russell need an additional 1.5% increase to fully recover those losses.

What conclusions can a professional investment advisor or individual investor draw from these numbers? Those who follow their own strategic analysis — rather than the negative, often biased narratives pushed by various media outlets — will observe that

the Trump administration is, in our view, acting on a clear plan with a strict timeline and aiming for tangible, long-term results.

So far, only one of many anticipated trade negotiations has concluded — and arguably the most important one: with China. If finalized successfully, this agreement could trigger many more, due to its scope and significance for global trade.

Despite ongoing challenges — including the situation in Ukraine and interest rate uncertainty — U.S. indices continue their upward trajectory based solely on recent developments. We believe this positive momentum will persist, as these steps are being perceived as a shift toward a more pragmatic and mutually beneficial tariff policy by the U.S. government.

Positive sentiment is also reflected in equity capital inflows and the strengthening of the U.S. dollar, driven mainly by demand for American assets.

After months of consolidation around the $60 level, crude oil has begun an upward move, with initial resistance at $67 and the next target at $73. Simultaneously, recent macroeconomic indicators contradict recession forecasts and are laying the groundwork for further positive moves — potentially even an interest rate cut by the Federal Reserve. We do not expect the Fed to remain long in rhetorical opposition to President Trump’s stance. In fact, we may see a shift in tone during Chairman Powell’s upcoming speech regarding whether high interest rates should persist. Ahead of that, we await the release of two key indicators: CPI and PPI, both of which are expected to support a positive economic outlook.

If the pace of negotiations accelerates, we may see U.S. indices return to positive territory for the year sooner than expected — perhaps even test the annual highs last seen in late January.

As we’ve previously highlighted, many stocks were trading at attractive valuation levels that couldn’t go unnoticed — and indeed, they did not. However, plenty of sectors still offer substantial discounts and remain poised to benefit from the next upward phase.

Feel free to contact us or the team at Maritime Economies for more information on these opportunities. As an investment advisor, I strongly believe that opportunities are always present — but sometimes, the timing is what makes all the difference in realizing exceptional returns.

by Kotsiakis George