The global economy is no longer moving through a simple post-pandemic adjustment. It is transitioning into a new strategic cycle shaped less by short-term macroeconomic fluctuations and more by deep geopolitical and financial realignments. In recent weeks, markets have sent clear signs that the next investment phase has already begun quietly beneath the surface.

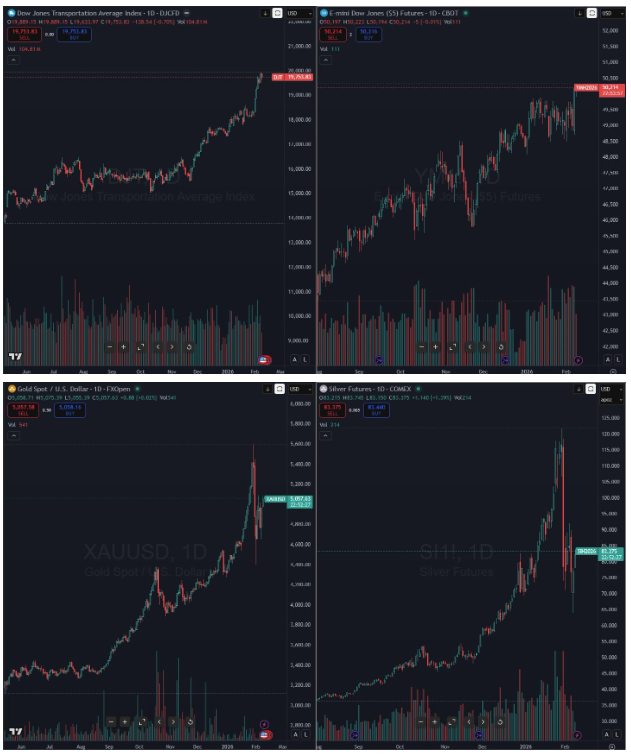

The fact that equity indices are trading near new highs while gold, silver and more speculative assets correct sharply is not a contradiction. It is an early sign of capital reallocation. Positions built on fear and inflation hedging are gradually being replaced by investments in the real economy and in sectors linked to trade, transportation and infrastructure. This is not the behavior of a market preparing for collapse, but of one preparing for a restart.

At the same time, global debt levels remain at historic highs. With sovereign and corporate balance sheets heavily burdened, the system requires nominal growth and stable or rising asset values to remain sustainable. In such an environment, deep and prolonged market declines become economically and politically difficult, increasing the likelihood that the coming years will be defined by managed expansion and periodic volatility rather than systemic contraction.

Geopolitics is accelerating this transition. The recent electoral outcome in Japan and the emerging direction of fiscal expansion is creating a new wave of liquidity and capital flows across Asia, at a time when global supply chains are already being reshaped. Recent geopolitical instability, rather than acting as a deterrent, has contributed to a new reconfiguration of maritime routes and a reassessment of freight market dynamics.

These developments confirm the assessments we have been presenting since early 2025. At the 17th Shipping Congress, we highlighted that shipping was set to enter a multi-year upward phase, a new “golden era” for the sector, at a time when the Baltic Dry Index was below 1,000 points and investor sentiment remained cautious. Our view was based on the expectation that the next major move would begin from a phase of accumulation and repositioning before the broader multi-year advance.

In early 2026 we reiterated this scenario when the Baltic Dry Index corrected again below 1,700 points, noting that a return above 2,000 would serve as clear confirmation of the next major upward phase, with potential continuation toward new historic highs in the years ahead. This move is already beginning to confirm itself, as recent momentum suggests the market is reclaiming its long-term upward trajectory.

Similar signals are appearing across other key indicators we closely monitor. The Dow Jones Transportation Index reached new all-time highs several sessions before the Dow Jones itself achieved new record levels, reaffirming that the transportation and logistics sector continues to lead broader markets and act as a precursor of the next economic phase.

Shipping once again stands at the center of this transition. Historically, maritime markets move ahead of broader economic cycles, responding first to shifts in trade flows, infrastructure investment and geopolitical balance. Current conditions reinforce the view that the sector is once again acting as an early indicator of a new multi-year expansion phase. The volatility of freight rates that defined the previous period is gradually giving way to a more mature environment in which demand linked to reconstruction, energy, evolving trade routes and technological infrastructure upgrades will become the primary driver of profitability.

Capital market behaviors support this picture. There is no broad liquidation of risk assets; instead, a reallocation of capital is underway. Large pools of liquidity remain in cash and money market funds, waiting for clarity on interest rates and geopolitical stability. When that clarity emerges, these funds are likely to move first into the real economy.

A development of particular importance for the investment community is the liberalization of access to the Saudi Arabian stock market. The removal of previous restrictions opens a market with capitalization exceeding $1.5 trillion to a far broader range of investors, creating new opportunities for positioning and strategic partnerships. This market is closely tied to energy, shipping, infrastructure and the Middle East’s technological transformation, making it one of the most significant investment hubs of the coming decade.

Its Sunday trading schedule, ahead of the opening of global markets, allows it to function as an early indicator of capital flows and geo-economic expectations, potentially transforming it from a satellite market into one that anticipates global developments.

The confirmation of our assessments is now evident. The movements of the Baltic Dry Index, the early breakout in the Dow Jones Transportation Index and the ongoing shift of capital toward the real economy all indicate that a new investment cycle is already taking shape.

For investors, the window of opportunity remains open but limited. If major technology companies have not yet fully assumed leadership of their next upward move, outperformance continues to emerge in sectors connected to shipping, energy, transportation, infrastructure and the broader geo-economic realignment.

This is not simply another upward cycle.

It is the beginning of a new era.

And those who recognize it early will be the ones who shape the returns of the years ahead.

by Kotsiakis George