The continuation of the second half of 2026 finds the global investment community facing a seemingly contradictory backdrop. If one limits themselves exclusively to the nominal values of the major indices from the beginning of July, the first impression is that of a corrective pullback, as surface-level nervousness shows Nasdaq and the S&P 500 under slight pressure. However, the true behavior of equity movements on the board reveals an entirely different reality. No signs of panic, mass liquidations, or generalized flight to cash are recorded on the board; on the contrary, the markets are undergoing a fierce, structural rotation beneath the surface.

This technical restructuring is directly fueled by the new, stringent reality introduced by the new Federal Reserve Chairman, Kevin Warsh. In his recent, highly anticipated appearance at the ECB Forum in Sintra, Warsh broke with years of tradition, categorically refusing to provide any forward guidance regarding upcoming interest rate moves, while simultaneously making it clear that the Fed will remain completely independent of political pressures from Washington. This lack of a pre-planned direction forces capital to become exceptionally selective.

This movement, however, constitutes a negative vote against the giants of high technology. The seven mega-cap tech companies (Magnificent 7) fully maintain their potent fundamental elements, their monopolistic advantages, and their absolute dominance in the structural super-cycle of Artificial Intelligence. What is being observed is a perfectly healthy, technical unwinding and controlled profit-taking following an explosive first half. The liquidity released from there is moving directly and methodically toward the real, cyclical economy, value sectors, and industrials, allowing the Dow Jones to sustain itself with remarkable resilience around the historic milestone of 53,000 points.

This invisible reallocation of wealth on the board finds its institutional validation in the rapid geopolitical developments of the NATO Summit in Ankara. The Summit serves as the central catalyst that legitimizes the transfer of money toward the sectors of physical infrastructure and security. The news flow reveals the scale of the diplomatic tension: European allies, under the weight of intense pressure from Donald Trump for immediate burden-sharing, initiated a coordinated "charm offensive," preparing a new naval mission for the permanent safeguarding of the Strait of Hormuz, confirming the close link between geopolitical stability and global trade flows.

The investment blueprint for the next decade was formalized by the Alliance’s Secretary General, Mark Rutte, who requested specific plans from member states for a binding transition of defense spending to 5% of GDP by 2035. Already, within the framework of the Defense Industry Forum in Ankara, massive defense contracts worth tens of billions of dollars were announced, such as the procurement of Northrop Grumman’s Tritons for maritime surveillance, the official selection of Saab’s GlobalEye for air defense, and the Drone Edge initiative. The immediate surge of defense stocks on the board, with Saab recording a jump of over 5%, stands as living proof that smart money faithfully follows sovereign capital flows.

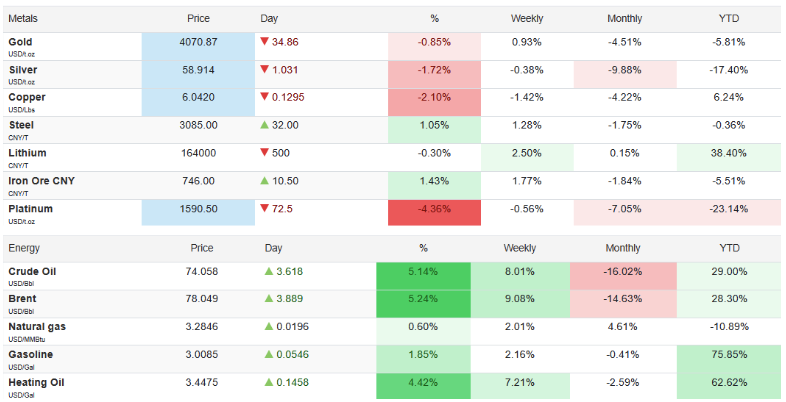

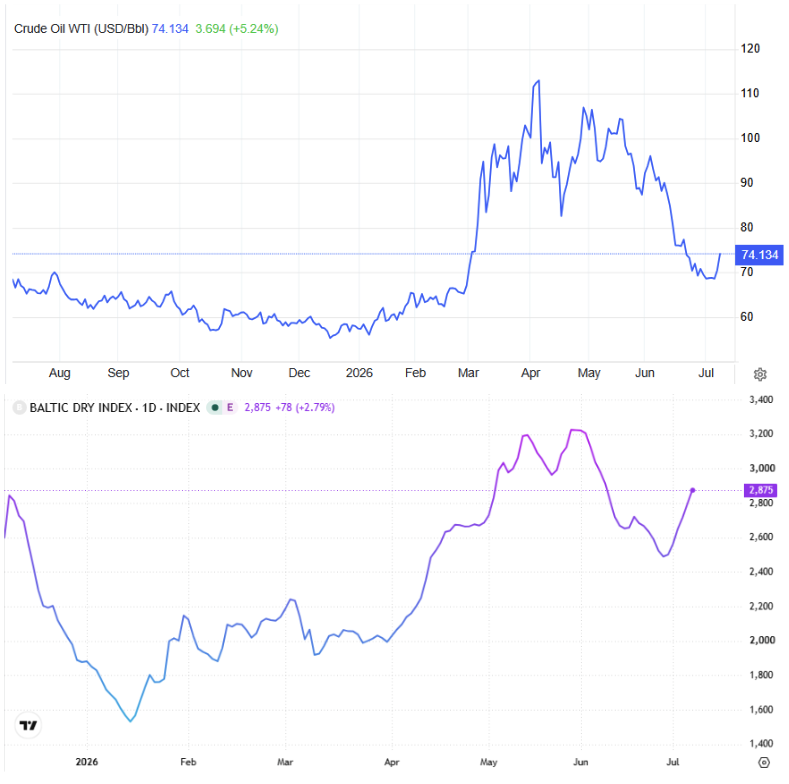

On the energy front, the naval safeguarding of the Straits fully reinforces our macroeconomic scenario. Even though oil may exhibit short-term, technical upward reactions, temporarily remaining above 70 dollars, the strategic position of GEKODESK & PARTNERS is clear: we expect a return of prices to the 60-dollar levels and potentially even lower in the coming period. This structural unwinding is expected to drag down refined products as well, with Gasoil steadily heading toward a return close to the 700-dollar levels, offering massive cost relief for industry and transport.

This geopolitical necessity for safeguarding logistics and maritime trade lanes triumphantly validates our own long-term strategic position. When the market watched the Baltic Dry Index (BDI) temporarily retreating, GEKODESK & PARTNERS maintained with institutional consistency that its return above the psychological and technical threshold of 3,000 points was merely a matter of time. This movement has already begun dynamically, with the BDI rebounding strongly toward 2,717 points, sealing a cumulative plus 77% YTD. Driven by the return of major charterers to dry bulk and robust demand for tons-miles, this recovery establishes the shipping sector as a permanent pillar of guaranteed flows.

In the currency market, these developments fully vindicate our consistently negative stance on the euro. Europe, trapped in its anti-Russian policy from the onset of the war in Ukraine until today, has only managed to dramatically bloat its bill of sovereign expenditures, at the exact time its economy is sliding into the path of a deep recession. This explosive cocktail of fiscal burden is expected to magnify even further under the strategy of Donald Trump.

The confirmation that Europe will entirely shoulder the new €70 billion package for Ukraine without US participation, combined with the forced funding of mega εξοπλιστικών programs for 5% of GDP, starves real growth of valuable resources and pressures the Eurozone's deficits. On the flip side, the US dollar retains the absolute advantage, with the DXY index moving steadily above 101, as the absence of forward guidance from Kevin Warsh serves as a reminder that US interest rates will remain high for a longer period.

The current juncture reaffirms our core philosophy. The nervousness of the general indices at the start of the month does not represent a sign of weakness, but a necessary rebalancing of positions. The technological giants remain the locomotive of global growth, yet smart money is simultaneously positioned where new geopolitical needs dictate long-term industrial investments. In such an environment, passive exposure to general indices (indexing) lacks strategy. Success in the second half of the year, ahead of the Q2 corporate earnings starting on July 14th, will be judged exclusively by the ability to read these internal rotations of capital early, maintaining composure, and balancing between technological supremacy and geopolitical reality.

by Kotsiakis George